Moonwell left unbacked due to Nomad hack, Aave proposes to freeze Fantom markets, PoW ETH potential effects on L2s lending, An interview with Euler CEO...

Moonwell left unbacked due to Nomad hack, Aave proposes to freeze Fantom markets, PoW ETH potential effects on L2s lending, An interview with Euler CEO...

Issue #5 of The State of DeFi Lending newsletter

Welcome to issue #5 of The State of DeFi Lending, a newsletter covering the highlights of lending markets in DeFi.

In this issue we cover

The Moonbeam network resumed operations post Nomad hack, but its biggest lending platform remains insolvent.

Risk DAO observes the upcoming ETH fork potential effects on the stability of L2s lending platforms.

Aave proposes to freeze its v3 Fantom markets.

MakerDAO discusses PoW ETH risk impacts.

An interview with Michael Bentley co-founder of Euler Finance.

Read below for more…

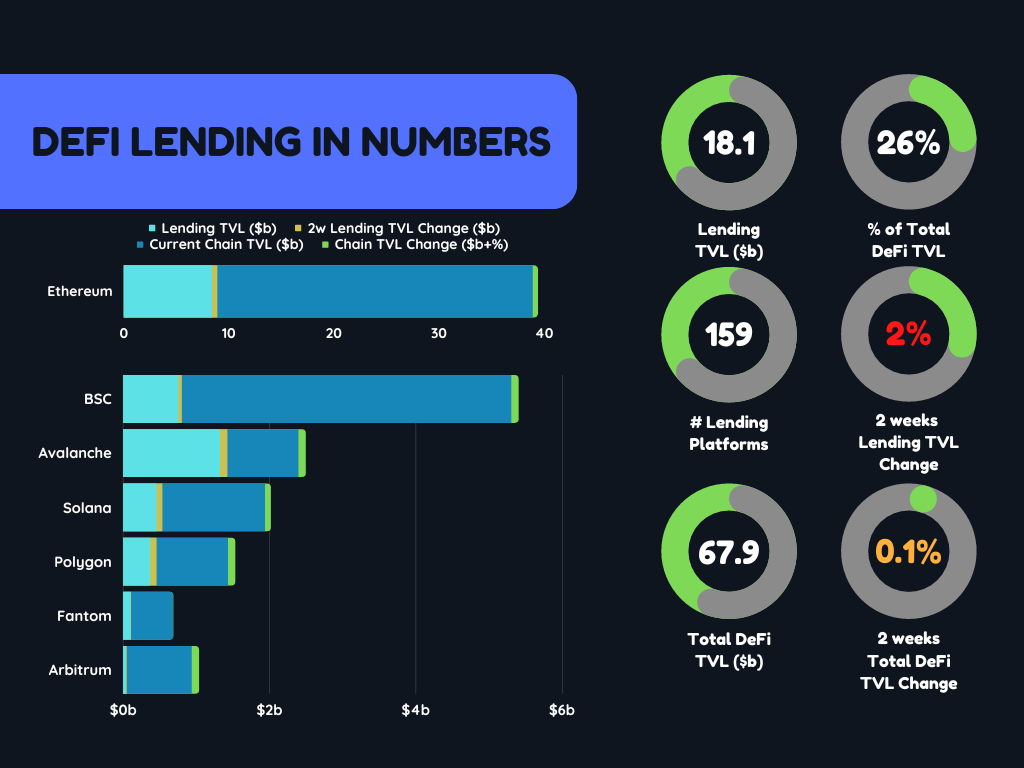

Very small changes in DeFi lending TVL and in general TVL in DeFi during the last 2 weeks. Fantom got shrunk, while other chains grew slightly. Ethereum lending grew roughly 3%, adding ~$325m, while Arbitrum nearly tripled its lending TVL, rising from ~$50m to $130m in lending/borrowing activity on the network.

News Recap

Moonwell becomes insolvent as Nomad bridge is still seeking for hacked funds

On August 2nd, a “mass” hack took place, gobbling up $190m of funds from the Nomad bridge. A misconfiguration in one of the recent upgrades of the bridge left a window open for anyone to copy-paste transactions in a way that drained the bridge. Samczsun gave a technical overview of the hack, but the bottom line was more straightforward -

Moonwell, the biggest lending market on Moonbeam (pre-hack), was left with unbacked assets that were originally bridged from Ethereum mainnet, which now got drained.

Though being punished for nothing wrong in their own code, the Moonwell team has not shared a lot of info on the case as the only “official announcement” that is linked on the lending platform app directs to a somewhat laconic tweet regarding the pause of the Moon Harvest campaign, a liquidity mining program ran by Moonbeam.

DeFi has seen some magnificent recoveries in the past, including in the last bull run, but only time will tell if the bear market can hold up similar resurrections.

Risk DAO points out some potential ripple effects of PoW ETH on L2s and alt-L1s lending markets

As the Ethereum merge is getting closer, it seems the option for a PoW ETH fork to get support from miners is becoming more realistic, with some already announcing they will maintain ETH1 chain (PoW ETH or ETHW).

This may affect lending markets on L2s and alt-L1s before the merge in 2 separated, yet related scenarios. In the first scenario, ETH on L2s/ Alt-L1s will be traded with a significant discount w.r.t mainnet price because their users won’t be eligible for PoW ETH. As Chainlink will still quote ETH price on L2s according to its price on mainnet (as it should), the price oracle will deviate from real L2s DEX price, making liquidations fail in case the deviation is greater than the liquidation penalty (changing from platform to platform but usually around 5-10%).

In the second scenario, PoW ETH has some non-zero value predictions which drive ETH holders on L2s to bridge their ETH back to mainnet to be eligible for the upcoming “airdrop”. This will create a liquidity contraction on L2s, making it hard to execute liquidations of underwater positions via L2s’ DEXs.

The likelihood of the first scenario is probably smaller than the second one, but the ability to mitigate the second scenario risk, by having bridges supporting PoW ETH redemptions, will be hard to implement in the short time frame before the fork. Some bridges have already mentioned their strategy toward the fork.

In both cases, the Risk DAO predicts that these effects are probably short-term and things are expected to get back to normal after a (potentially chaotic) start in the days or weeks after the merge.

Hasu made a clear point about the buzz around PoW ETH.

Aave’s proposal to freeze Fantom markets on its v3 is getting mixed reactions

The recent Nomad bridge hack, and the Horizon bridge hack that took place in June, were the alleged reason for a proposal made on the Aave forum last week to freeze the Fantom markets on Aave v3, citing the main cause as the low traction that does not match the potential risk in case the Fantom bridge will be hacked as well.

For those following our newsletter, it doesn't come as a surprise that Fantom lending activity, like its entire ecosystem TVL, has shrunk significantly in recent months.

Still, some have taken the time to do the math to check if the so-called risk/reward ratio that was the main reason for the proposal is unique to Fantom, just to discover it isn’t, also clarifying that the same Anyswap bridge is used for other networks as well -

In a Twitter response, Marc Zeller who proposed the freeze made it clear(er) that the future of alt-L1s relays on Avalanche and Polygon -

At the time of writing, there is no date for the Aave proposal to go live for a vote.

MakerDAO discussing potential risks and required mitigating actions for the upcoming ETH fork

As discussions are evolving on PoW ETH being maintained by miners to extract some value as long as they can, MakerDAO is discussing the required actions that need to be taken in order to mitigate the risks while keeping Maker competitive in the ever-changing DeFi lending environment.

Maker’s risk unit contributor Monet Supply, acknowledges a long list of risks on Maker’s forum, 3 of them covered in a somewhat more concise version over Twitter -

As for now, these seem more like preliminary monitoring steps rather than an active governance proposal taken by MakerDAO in order to remain vigilant on any changes in the lending markets as the fork/merge is getting closer.

5Qs

For our #5 issue, we are excited to have Michael Bentley, co-founder of Euler Finance and CEO of Euler XYZ, the development company behind Euler, answering our 5 questions (and it’s pronounced Oiler!)

1. Current DeFi lending platforms are either based on open market interest rates (e.g., Compound, Aave and Euler) or on a debt-backed stablecoin with an interest rate that is set by the protocol governance. Where is the catch/magic in stablecoin that allows them to set arbitrary interest rates, and can lending platforms benefit from launching their own stable coin? Does Euler have plans to launch a stable coin?

Lending protocols and stablecoin protocols both derive a lot of their present day use-cases from a demand for leverage among their users. Specifically, users will often deposit collateral (e.g. ETH), borrow another asset (e.g. DAI or USDC), swap it for more collateral, and repeat the process. In the end, they have a leveraged long position on the collateral they started with (and a short position on the asset they borrowed).

One of the main differences between these two routes to get leverage is in the supply of the borrowed asset. On a general lending protocol, the borrowed asset has a finite supply, whereas on a stablecoin protocol, the borrowed asset (e.g. DAI) is minted at the time of borrowing. This creates some interesting trade-offs.

The upside of the general lending protocol is that the borrowed asset always has some pre-existing external demand that is unrelated to the lending protocol. So swapping it on a secondary market for more collateral is easier.

The downside is that if the asset has a finite supply, it also has a finite supply of lenders (which is only ever a subset of all possible holders). This means that borrowing costs may be expensive. They will always reflect the wider market conditions.

The upside of a stablecoin protocol is that the borrowed asset has a potentially infinite supply (depending only on the amount of collateral accepted). In some sense, there is no lender. Or, perhaps, one can think of users lending value to themselves. Because of this, the interest rate for borrowing a stablecoin asset could, in principle, be zero. In practice, the stablecoin protocol will often charge the borrowers a fixed rate of interest and use this elsewhere in the system. Crucially though, the interest rate can be fixed at a much lower rate than users on a general lending protocol would expect to receive (e.g. 1.5% fixed versus 0–5% variable).

The downside of stablecoins is that they need mechanisms in place to drive demand. The demand is needed so that users can perform the aforementioned swap in order to take on a leveraged position. Where does this demand come from? Well, it could come from other borrowers wanting to settle up their loans. For example, a user B who wants to settle up their loans might buy back their DAI from user A who is about to start building up a leveraged position. However, this matching alone is unlikely to create a sufficiently vibrant secondary market to enable a stablecoin protocol to survive. So additional mechanisms are generally needed to drive demand for the stablecoin. Once these additional mechanisms are in place, further mechanisms are generally needed to prevent the opposite problem: over demand. This last point is important because, in principle, there is nothing inherent about a stablecoin borrowing module that guarantees its price stability.

If a borrower sells a stablecoin for $1, then they will generally profit if they can buy it back for less than $1 (and repay their loans). This helps keep the price of the stablecoin from dipping too much below $1. They will generally make a loss, however, if they have to buy it back higher than $1. If demand for the stablecoin on the secondary market outstrips supply, it can lead to a short squeeze, where borrowers are forced to buy back their stablecoins at a higher price in order to repay their loans. More repaying drives up the price still further, leading to a spiral of pain for borrowers.

One way to curb demand for a stablecoin and prevent the spiral of pain is to create a route through which supply can be increased without further borrowing. This could potentially be achieved by, for example, minting more stablecoins when the price of the asset is above $1 and lending them out on the market. One approach for doing this might be via an integration with a general lending protocol. So there is an argument that there are unique synergies that might exist between general lending protocols and stablecoin protocols in terms of peg maintenance mechanisms.

Ultimately, my personal view is that stablecoin protocols walk a very fine line when they try to maintain a peg by layering in lots of additional mechanisms. These are complex dynamical systems, and it is not clear to me that we can predict their behaviour over the long term or even medium term. If one were to write this down as a system of equations and try to study what happens, you would have little chance of identifying all of its solutions. Protocol designers are relying heavily on their intuition about how first-order effects will impact the dynamics. But every new mechanism adds complexity and unpredictability. You get a combinatorial explosion of edge cases that need to be understood and guarded against.

All this being said, I think there is real magic in being able to create stable value systems out of unstable systems. Users wanting leverage end up paying a premium to create a stable and censorship-resistant asset that ordinary users can hold instead of local currencies that might be inflationary or at risk of being purloined.

2. In the traditional world, most of the lending activity is for fixed-rate/term loans. Why is this not the case for DeFi? Does Euler have any plans to support it?

Fixed-rate loans always involve users paying a premium to get a fixed rate of interest. One can think of the premium paid as a kind of insurance premium against interest rate volatility. I do think these kinds of loans have a big future in DeFi long-term. We have probably not seen as much growth in fixed-rate lending as variable rate for a few reasons. First, fixed-rate lending is something that typically gets built on top of a variable-rate system, and the latter hasn’t been around that long. So there is a technical delay in the development and iteration of these protocols. Second, fixed-rate loans need counterparties willing to bet on the state of interest rates and take on the risk. Any sensible counterparty of size would want to gauge how variable interest rates change over time in the long term and in different types of market conditions before wanting to enter that market. Third, at the moment there is largely only demand for borrowing to build leveraged positions in DeFi. These are inherently short-term in outlook. In traditional finance, fixed-rate products tend to be for long term loans, like mortgages. These will come to DeFi eventually, but are probably some time off for now.

3. Does Euler have a multichain strategy? E.g., Compound was extensively forked by other projects and recently introduced a Business Source Licence to mitigate forking. Does Euler work on something similar?

Euler was initially deployed on Ethereum L1 and currently is not being built for deployment on L2’s or other networks. I do think someone will propose this to the DAO someday and it will be interesting to see the response. I see this discussed fairly frequently in community channels. Personally, I feel strongly that rushing to deploy on other networks would not be good for Euler right now. When we deployed Euler initially, we did so in a risk-mitigated way, with limits on collateral and so on. This no doubt hindered growth of the lending markets, but we felt it was important to put security first. I think an even greater level of caution should be taken with new networks.

There are just too many things that can go wrong. Every network has its own risk properties that are unique to that network. There are many questions one needs to consider. How are user assets bridged? How do oracles work? How centralised is validation/mining of blocks? And so on. During the last year or so, there was a lot of hype around alternative chains and networks. But now that the hype has died down, we are starting to get a better view of which ones are here to stay with real users and use-cases.

4. MakerDAO governance is making decisions on a monthly basis and recently had a mini civil war. Compound governance, on the other hand, is taking relatively few decisions every year. What is your view on the ideal governance model for lending platforms?

Lending and borrowing protocols may require a stream of input from external users in ways in which something like a decentralised exchange typically does not. The code may not be able to be perfectly immutable, using only data internal to the blockchain to run securely.

To understand why, consider the question of whether or not USDT should be listed as a collateral asset in DeFi. Many people will have a visceral opinion on this question, all of which is probably based on their view about how an off-chain company, Tether, operates. Compare USDC to USDT on-chain, and it would be very difficult to design an efficient algorithm to capture the variety of people’s beliefs on this topic.

(For what it’s worth, I think USDT should be considered as collateral in DeFi today. However, my opinion on this has changed over the years as more information has become available and Tether has increased their transparency. Which helps to highlight why lending protocols need upgradeability. What is suitable collateral today may not be tomorrow, and vice versa.)

With this in mind, I do think governance needs to have some form of representation from people who hold detailed knowledge about how these protocols work and detailed knowledge of wider market risks. However, this raises difficult questions and challenges because if governance requires a smaller number of people to be involved in decision making, you have problems of centralisation, regulation, and even liability. This is complex stuff that is a long way from being resolved.

If governance token holders vote directly on every issue, you are likely to get problems of voter apathy, voters being misinformed about risks, voters being manipulated, and so on. If governance is run by smaller teams of specialised individuals, you potentially lose a degree of censorship resistance and even open up individuals to claims of liability for decisions (whether good or bad).

Overall, my broader view is that everything does not need to be ‘fully decentralised’ in order to support a decentralised web. People generally want reliable decentralisation as an option, not for everything to be 100% decentralised 100% of the time. If the base layer network is sufficiently decentralised, then the free market can choose what level of decentralisation it wants for a given purpose. If I’m trading a few dollars worth of a meme coin for fun, I would rather pay low fees on a centralised network and get speed of execution, than use an immutable protocol that charges higher fees and has slower execution times. If I’m based in an authoritarian country and worried about the safety of my families’ assets in the event I say something out of turn, I clearly care a lot more about decentralisation.

I agree with a recent post by ChainLinkGod in which they said that ‘DeFi’ was a poor choice of name for the umbrella of protocols being described as ‘DeFi’ protocols in the last few years. ‘On-chain finance’ is probably a better umbrella term that captures both the truly decentralised applications as well as the wider set of protocols and infrastructure around them that support the broader vision of web3. On-chain lending protocols may necessarily sit in a grey area, more towards the decentralised end of the spectrum, but not as far as immutable DEXs like Uniswap.

For people that desire truly immutable lending protocols, I think they will need to accept that such protocols can be designed only if you accept a much lower level of capital efficiency and/or higher levels of risk. Liquity is an excellent example of this. It accepts only ETH as collateral, which limits its capital efficiency, but allows it to operate in a standalone fashion. It also depends on oracles that cannot be upgraded, which adds an element of risk in the event they need fixing. Ultimately, it is up to the free market to determine what it wants.

5. Do you think DeFi lending will eventually become a winner takes all market with one big platform having 99% of the market?

No, I doubt it. There are too many trade-offs involved. Any lending protocol that tried to be the best of all things to everyone would probably be too complicated to be safely constructed. Security often comes from modularity and simplicity. Euler is extremely modular in design for this reason. But in general, there will always be people who want to earn higher interest for higher risk, and others who look for low-risk opportunities above all else. Today, Euler has fewer collateral assets than Compound and Aave. This places it among the lower-risk protocols for collateral risk. Yet, it also supports lending and borrowing for a much larger number of assets overall, which allows users to take advantage of higher risk strategies in an isolated risk environment if they want.