Special issue - A deep dive into Compound III, an interview with Jared Flatow of Compound Labs

Special issue - A deep dive into Compound III, an interview with Jared Flatow of Compound Labs

Issue #4 of The State of DeFi Lending newsletter

Welcome to issue #4 of The State of DeFi Lending, a newsletter covering the highlights of lending markets in DeFi.

In this issue we cover:

Compound III

An interview with Jared Flatow, VP Engineering at Compound Labs

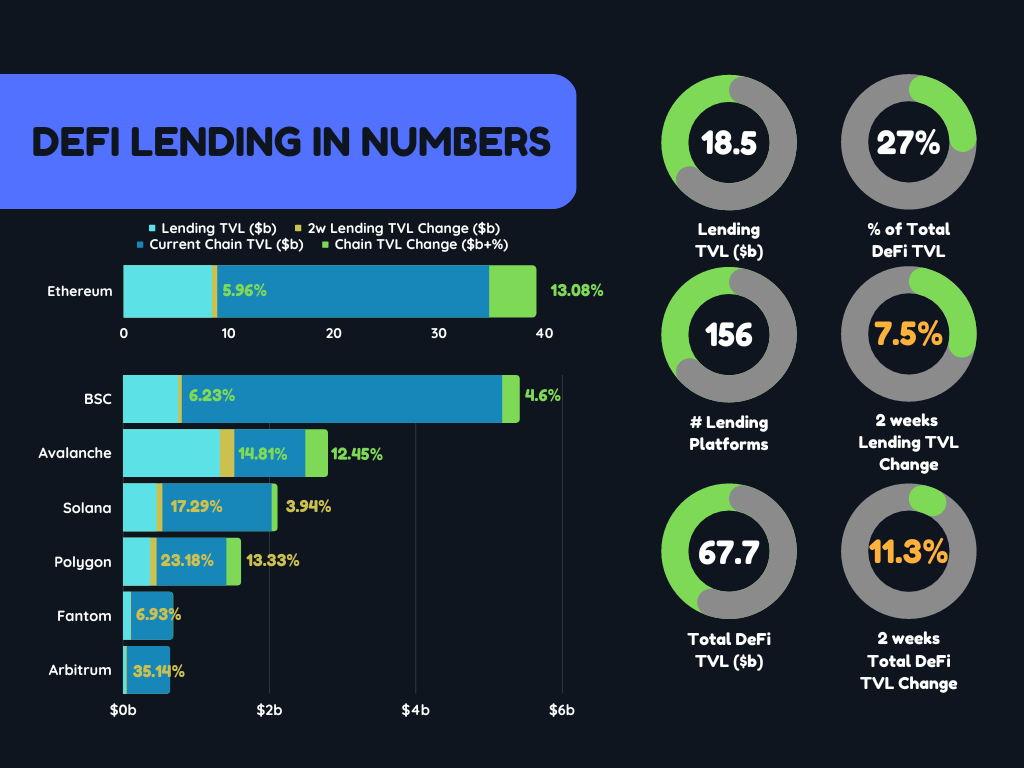

Even though Arbitrum has regained 35% of its lending TVL in the last 2 weeks (after dropping 76% in the previous 2 weeks), and Ethereum saw a rise of $4.5b in total chain TVL, the total lending TVL remains roughly at 27% of the total DeFi activity.

Compound III - overview

On June 29th, Compound Labs released a code repo to support Compound’s multi-chain strategy. After seeing many Compound forks successfully deployed on other chains, including BSC, Avalanche, Tron, Polygon, and others, Compound have taken the decision to support users’ demand for more affordable chains than Ethereum mainnet.

The announcement created some initial confusion as it didn’t mention the previous work made by Compound Labs on its multi-chain strategy - Gateway. Talking with the team at Compound Labs it was calrified that the work on Gateway has been put on hold due to the rapid growth in the multi-chain landscape in DeFi in the passing year.

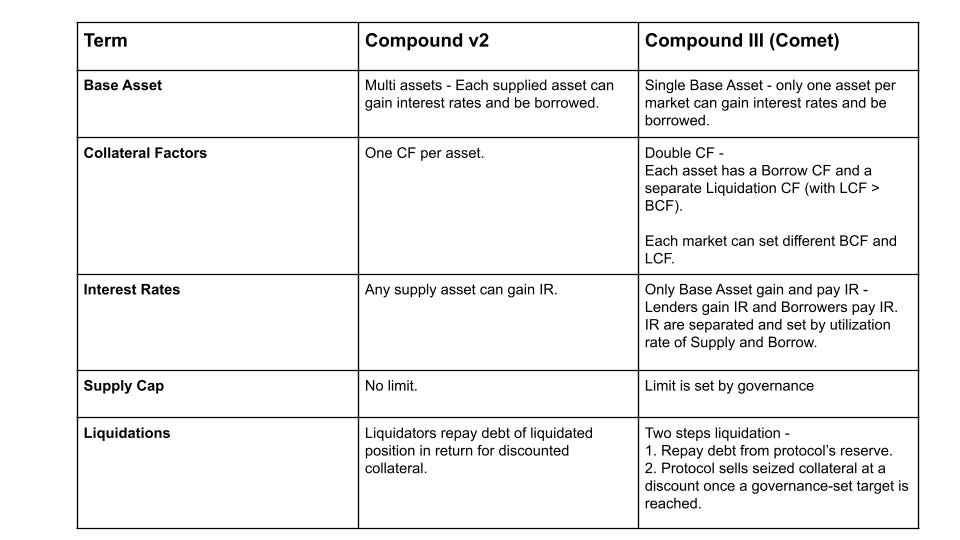

There are a few significant changes in Compound III worth noticing:

Single Base Asset - In Compound III, only one asset is borrowable in each market, making it a single base asset market. Other assets can be supplied as collateral to set the borrowing power of the account (according to the accumulated Borrow Collateral Factor of the supplied assets). Only the supplied base asset will earn Supply Interest Rates in Compound III and the only one users will pay interest for (e.g., no more APRs on parking your assets as collateral in Compound).

Having a single base asset separates the users of Compound into two clear segments - Lenders and Borrowers. Lenders will provide the single base asset to earn interest rate, while Borrowers will need to provide other collateral before being able to borrow the base asset (and paying interest for doing so).

Dual Collateral Factors - Comet presents two CFs, set separately. The first is the Borrow Collateral Factor and the second is the Liquidation CF, where LCF > BCF.

As Adam Bavosa, Developer Relations Lead at Compound Labs clarified over chat -

In Compound III, there are two separate collateral factors that borrowers need to consider. The Borrow Collateral Factor is a percentage of the collateral value (in USD) that the user may borrow. The user can borrow this entire amount at once and they will not be liquidated in the next block, which would be true in Compound v2. The Liquidation Collateral Factor is always higher than the borrow collateral factor. (Only) if a user's borrow balance accrues high enough to reach the value of the liquidation collateral factor, the account becomes liquidatable. So you can think of the gap between these collateral factors as a "no new borrows" period where the borrow is considered solvent and not yet liquidatable.

The complexity to set the right CF and other risk factors associated with multi-debt markets was recently assessed and covered in this Medium post by Yaron Velner, B.Protocol’s founder and a lead contributor to the Risk DAO

In short, the conclusion of the analysis shows that controlling the borrowed asset used against a specific collateral, like in Compound III, gives better control over the associated risk for the lenders, as well as set the opportunity for better capital efficiency for borrowers.

Supply Caps - Unlike in Compound v2, Compound III can set a maximum quantity of Supply per asset in each market, set by the governance (supplyCap). This was added as a way to mitigate risk exposure to specific collateral assets in the market, something that might be useful when deploying on L2s and alt-L1s, with the option to list riskier assets as collateral.

Liquidations - Compound III introduces a new liquidation mechanism where the process is being separated into two steps. Step 1) repaying the liquidated position debt from the protocol’s reserve while keeping the seized collateral in the reserve. Step 2) Kicks in once a threshold target of that specific asset in the reserve is reached. Once the target is reached the reserve asset will be offered to sell with a discount.

Separating the process absorbs some of the associated liquidation risk in 2 ways - 1) it creates a buffer between the current dex liquidity and the seized collateral which doesn’t need to be sold immediately, and 2) it off loads the lose potential, created by bad debt, from lenders to the protocol reserve itself (which is filled by borrowers’ reserve fees).

Browsing through Compound III docs, it seems the incentive to call the liquidation function will be given through “liquidatior points” that will be added to gas costs in what seems to be some sort of a token reward that might be distributed in later stages 🧐.

As for the multi-chain opportunities that stem from the solitary base asset markets, deployed across different chains, with bridging opportunities evolving all the time, it seems this is still “an open space for possibilities” yet to be explored by the community and future development according to Jared Flatow, VP Engineering at Compound Labs (see full interview below).

Here’s a “one-glance” table to summarize the main changes coming up with Compound III -

6Qs Interview

For this special issue on Compound III, we are thrilled to have Jared Flatow, VP Engineering at Compound Labs, who has agreed to help us dig a bit deeper into what’s coming up with the new Compound III, aka Comet.

Q1 - Comet is presented as part of the new multi-chain strategy of Compound. What is the multi-chain main enabler in Comet? Given that most multi-chain forks of Compound contracted significantly in the bear market, why is a multi-chain strategy needed?

The Comet protocol contract is designed to be an efficient building block which can be deployed on different chains to support common use cases and composability. The design is versatile, and has few moving parts, making it relatively simple for governance to manage. Supply caps, dual collateral factors, and a single base asset [see comments for further details and explanations on these terms] give governance the ability to safely deploy and control independent markets. We also built new tooling into the repository itself to help the community safely manage multiple instances of Comet across different chains. We don’t expect the bear market to last forever, and the cost of Ethereum mainnet is always going to be relatively expensive. We think the protocol should exist wherever users are, and there is user demand for faster and less expensive networks (albeit with the tradeoffs that come with those things).

Another key piece of Comet’s multi-chain enablement comes from the solitary ‘base asset’ in each deployment. Once a liquid interest rate market exists for the same base asset (e.g. USDC) on multiple chains, it is possible to combine the multiple markets into a unified liquidity pool, as the base token positions are designed to be transferable through bridges.

Q2 - The Business Source License gives the Compound community the option to franchise the brand. This allows new deployments to either be independent and pay some fees, or another form of contribution to the Compound community, but potentially also to just mirror the Comp voting rights to the new chain, and give the Compound community full control on the new deployment. Are any of the options more native to the Comet implementation? Do you expect one of them will be more popular than the other?

The additional use grants are more exceptional and require explicit governance approval to deploy in a way other than being managed directly by the DAO. We wanted to support those grants in order to be flexible for future use cases which we hadn’t necessarily envisioned, but at this point we’d expect the community to take responsibility for the various deployments. We want to make it clear how a deployment can be compliant with the license, and what the path looks like to be officially adopted by governance. We are in the process of demonstrating what we expect that to look like on some of the larger networks as we speak.

Q3. One of the major changes in Comet, is that it supports only a single borrowable asset. Can you explain to the readers how this design option improves the market’s risk management? Why did you choose to continue support for multi collateral markets? Do you envision the main usage will be single collateral (other than the borrowable asset) vs single borrow?

By only having a single borrowable asset, the collateral factors are directly tied to the base asset. Compared to v2, the collateral factors can be higher for a given collateral, since the price risk is with respect to a particular asset, and in the case of a stablecoin that risk is completely a function of the collateral asset. We think multiple collateral assets is natural and improves flexibility for users and composability for other contracts and protocols.

A single base asset per market means that users get to control how much of each specific asset is borrowed against their supplied collateral. It means that governance can cap how much collateral of each type can be used to borrow each base asset. It also means that suppliers of the base asset have more control over their risk profile.

Q4 - Another major challenge in multi-chain and L2s deployments is lower DEX liquidity for liquidations. Comet introduces an improved liquidation mechanism. Can you explain to the reader how the new mechanism works, and why it is better?

It’s true that DEX liquidity is an important consideration when listing an asset on any chain. The new liquidation mechanism doesn’t remove the need for governance to take this into account when supporting an asset. The new liquidation mechanism splits liquidation into two independent steps: absorption of debt and the purchasing of collateral assets. Whenever an account is underwater, anyone may make a call to ‘absorb’ and transfer the position to the protocol. The protocol repays the debt plus additional reserves to the account, in proportion to the collateral being seized. The collateral may then be purchased from the protocol by liquidators, for a discount relative to the current oracle price. Since the protocol is always willing to transfer the debt to its own balance sheet, the safety of the protocol is directly protected by the reserves of the protocol.

Q5 - What type of new integrations and innovative “lego blocks” can you foresee enabled by the new account management tools Compound III will offer?

The new account management system effectively allows a user to delegate (or revoke) the ability for all its positions to be managed by another contract (or address). This is an extremely flexible mechanism, which enables all kinds of protocols to be built on top of the core protocol. We built our own ‘bulker’ contract functionality using this, which enables users to supply multiple assets and borrow in a single transaction, as well as the ability to supply ETH (on Ethereum) and wrap it with the requisite ERC20 (WETH). Removing the dependency on `msg.sender` opens up endless possibilities for integrations: for instance one could imagine an L2 protocol which allows users the ability to completely manage their positions off-chain. This system could be combined with new primitives the service provides or creates on or off-chain.

Q6 - It seemed like, at least a few, got confused regarding the development efforts made by Compound Labs on Gateway (aka Compound Cash) and the announcement of Compound V3 launch. Can you describe the main differences between the 2 products and what will set the right grounds for going live with Gateway?

From the time we wrote the Gateway/CASH whitepaper until the time we began work on Compound III, the multi-chain space evolved dramatically, with a number of bridges and other networks going live and with the continued proliferation of EVM-like chains. The Comet contracts attempt to distill much of what we learned in designing CASH and launching the Gateway testnet into an efficient, portable, self-contained protocol which could be deployed on any EVM-like chain. For the time being, any plans around Gateway and CASH are on hold, while we focus on helping the community bootstrap the new protocol on many chains. Connecting the Comet protocol instances together via a Gateway-like chain may be a future path towards shared liquidity for Compound instances, but not something we are actively working on at the moment.